Exclusive: Continuing Investigation Uncovers More Decade-Long Transparency Issues in Property and Mortgage Disclosures

Just when we thought we had uncovered the full extent of New York Attorney General Letitia James’ financial disclosure irregularities, our continued investigation has revealed yet another layer of troubling inconsistencies. We initially examined both of her properties simultaneously, but as our investigation progressed, we’ve uncovered increasingly concerning details that paint a more troubling picture with each new discovery—a pattern that traces back to 2013.

A Tale of Two Properties: Compounding Disclosure Problems

Our previous investigations uncovered serious questions about Letitia James’ Virginia investment property and her Brooklyn rental property. Now, a detailed examination of her Brooklyn property mortgage disclosures reveals an equally concerning pattern of delayed reporting, disappearing mortgages, and unexplained changes. The combined evidence paints a troubling picture of systemic financial disclosure irregularities across her entire real estate portfolio.

Legal Disclosure Requirements

Under Section 73-a of the New York Public Officers Law, elected officials like James are required to file sworn annual statements with the New York State Commission on Ethics and Lobbying in Government disclosing all real estate holdings (except personal residences that don’t generate income), all sources of income exceeding $1,000, and all debts exceeding $10,000. These aren’t optional formalities but legal statements signed under penalty of perjury.

False statements can constitute a Class A misdemeanor under New York law, punishable by up to a year in jail. The law states: “A reporting individual who knowingly and willfully fails to file an annual statement of financial disclosure or who knowingly and willfully with intent to deceive makes a false statement or gives information which such individual knows to be false on such statement of financial disclosure… shall be guilty of a class A misdemeanor.”

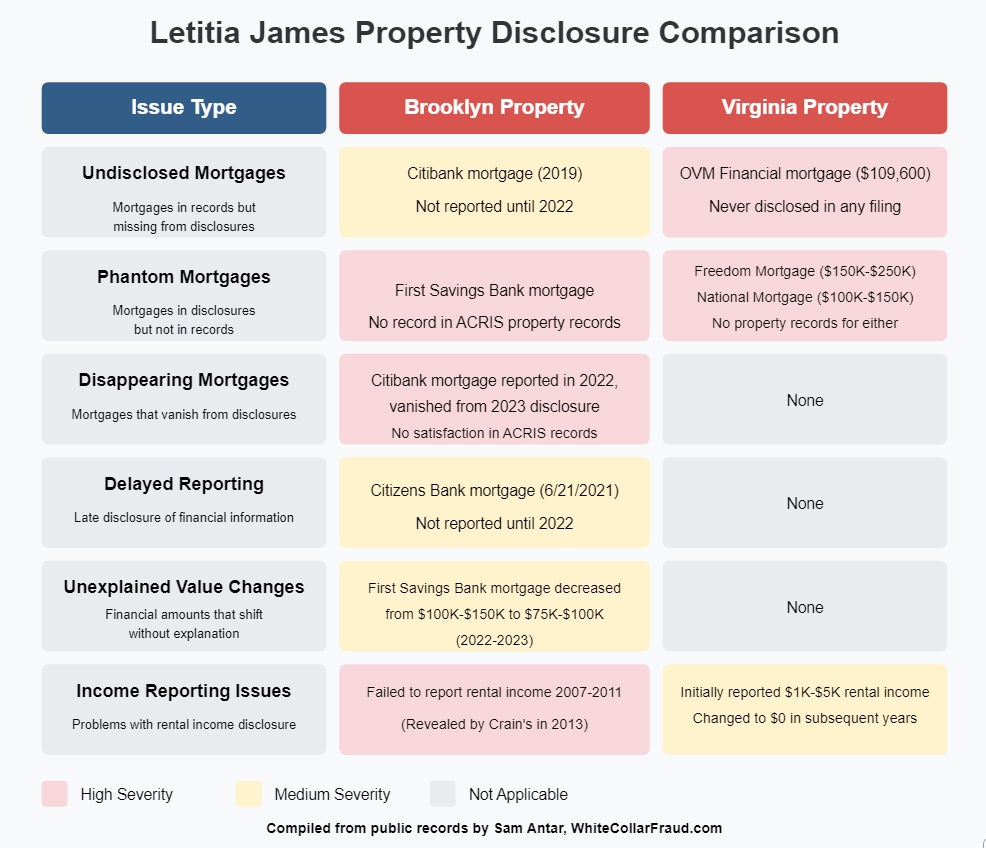

The Brooklyn Property Mortgage Maze

Public mortgage records (ACRIS) compared against James’ financial disclosures from 2020-2023 show several critical inconsistencies:

The First Savings Bank Mystery Mortgage

One of the most troubling discoveries is the First Savings Bank mortgage that James has consistently reported on her financial disclosures since at least 2020. Despite an exhaustive search of ACRIS records, we could find no trace of this mortgage in any official New York City property records. This raises serious questions about the existence and nature of this financial obligation.

Adding to the mystery, James consistently reported this mortgage in the range of $100,000-$150,000 for three consecutive years (2020–2022), but then in 2023, the reported value inexplicably drops to $75,000-$100,000 without explanation. While this could potentially be related to payment of principal, the absence of any official record of this mortgage in ACRIS makes it impossible to verify the actual terms, origination date, or even existence of this substantial financial obligation.

The Case of the Vanishing Citibank Mortgage

Perhaps equally troubling is the Citibank mortgage. According to ACRIS records, this mortgage was recorded on August 29, 2019. Yet it doesn’t appear in James’ 2019, 2020 or 2021 financial disclosures. It suddenly materializes in her 2022 disclosure—approximately three years after the fact—only to completely disappear from her 2023 disclosure.

This raises serious questions: Why wasn’t this mortgage reported for nearly three years? And why did it suddenly vanish from her 2023 disclosure?

The Delayed Citizens Bank Mortgage

The pattern continues with a Citizens Bank mortgage. ACRIS records show this mortgage was recorded on July 9, 2021. Yet James’ 2021 financial disclosure—which would have been filed after this date—makes no mention of it. The mortgage only appears in her 2022 disclosure, approximately a year late.

The Missing Mortgage Mystery

Follow the paper trail of James’ Norfolk, Virginia investment property, and you’ll encounter another puzzling contradiction.

Official property records tell one story. In August 2020, James purchased the modest home for $137,000. She financed it with a $109,600 mortgage from OVM Financial. The mortgage documentation classified it as a second home, with a specific “Second Home Rider” containing legal attestations about occupancy, though lenders typically allow conversion to investment properties with proper notification.

Her sworn financial disclosures tell another story entirely. From day one, she listed the property exclusively as an “investment” generating rental income. But the mortgage that made the purchase possible? It vanished completely – never appearing on a single financial disclosure despite clear legal requirements to report all mortgages on investment properties.

The mystery deepens in her 2023 disclosure. While the property’s value remains unchanged at “$100,000-$150,000,” two entirely new mortgages suddenly materialize:

- Freedom Mortgage ($150,000-$250,000)

- National Mortgage ($100,000-$150,000)

These loans could total up to $400,000 – potentially four times the property’s lowest declared value. Combined with the undisclosed but documented OVM loan of $109,600, the total debt could reach up to $509,600 against a property she valued at no more than $150,000. Yet our commissioned title search found no trace of either mortgage in any public records.

The property that once generated $1,000-$5,000 in rental income during 2020, now reportedly generates $0 – despite supposedly carrying up to $509,600 in total debt. As of 2025, Norfolk tax assessors value the property at just $187,300.

Even using this higher assessment, the loan-to-value ratio could be as high as 272% (considering all three mortgages totaling $509,600) – far exceeding the industry standard 70-80% maximum for investment properties. This type of loan-to-value ratio would be virtually impossible to obtain through legitimate lending channels.

The Pattern: A Side-By-Side Comparison

Below, is a side-by-side comparison of disclosure issues with James’ Brooklyn and Virginia properties, highlighting phantom mortgages, undisclosed debts, and reporting inconsistencies. Note that the Citibank mortgage vanished from her 2023 disclosure with no satisfaction reported in ACRIS property records.

A Decade Earlier: The Same Pattern

If these were isolated incidents, one might attribute them to administrative oversights. But our investigation uncovered an eerily similar situation from James’ past.

In May 2013, Crain’s New York Business revealed that then-Councilwoman James had failed to disclose rental income from her Brooklyn brownstone – despite collecting “tens of thousands of dollars every year” from tenants.

The four-story Lafayette Avenue property, purchased in 2001 for $550,000, had housed multiple tenants for years. Public records showed renters registering to vote at the address as early as 2001. Yet James’ financial disclosure reports between 2007 and 2011 made no mention of this substantial rental income, despite city laws explicitly requiring elected officials to report such outside income.

When confronted, her spokesperson claimed she was “previously unclear about whether owner-occupied rental income was subject to council disclosure.” After the Crain’s report, James hurriedly filed an amended disclosure – but even this correction understated her actual rental income of $44,400, reporting it instead in the “$5,000-$43,999.99” range.

That same year, another Crain’s investigation discovered James had underreported her campaign spending by 50% during a two-month filing period. “One neutral observer of the race suggested… that Ms. James’ campaign might have left off a number of expenditures from her original filing in order to minimize from public view her already high campaign burn rate,” Crain’s reported.

Timeline of Disclosure Issues

- 2001: James purchases Brooklyn property

- 2001-2011: Tenants live in Brooklyn property

- 2007-2011: James fails to disclose rental income from Brooklyn property

- 2013 (May): Crain’s reveals James failed to disclose rental income

- 2013 (May): James amends disclosure but understates rental income

- 2013 (April): Crain’s reveals James underreported campaign spending by 50%

- 2019 (August): Citibank mortgage recorded but not disclosed until 2022

- 2020 (August): James purchases Virginia property with OVM Financial mortgage

- 2020: James reports Virginia property as investment but fails to disclose OVM mortgage

- 2021 (July): Citizens Bank mortgage recorded but not disclosed until 2022

- 2021-2022: James reports 42% value increase in Brooklyn property while city assessment shows 7.6% decrease

- 2022: James reports Citibank mortgage three years after origination

- 2023: Citibank mortgage disappears from financial disclosure without explanation

- 2023: James reports two mortgages on Virginia property (Freedom and National) that don’t appear in property records

The Unanswered Questions

As James pursues others for financial misrepresentations, her own disclosure history raises troubling questions:

- Why does the First Savings Bank mortgage appear in her Brooklyn property disclosures since 2020 but not in any official ACRIS property records?

- Why is the only mortgage that appears in Virginia property records (OVM Financial, $109,600) completely absent from all of her financial disclosures?

- Where did the two mortgages reported in her 2023 disclosure for the Virginia property come from, and why don’t they appear in any property records?

- How could a property generating no income secure mortgages totaling up to $509,600?

- Why did she sign a document legally attesting the Virginia property would be a second home, while simultaneously reporting it as a rental investment?

- Why has James reported $0 in rental income from her Norfolk property in recent disclosures, despite initially reporting $1,000-$5,000?

- Given her history of failing to disclose rental income from her Brooklyn property for years until media scrutiny, is this another case of unreported income?

- How could someone with legal training repeatedly fail to accurately report basic financial information across multiple properties and multiple years?

The Standard Bearer’s Double Standard

The irony is inescapable. As New York’s chief legal officer, James has built her reputation on holding others accountable for their financial disclosures. Her $355 million judgment against former President Donald Trump centered on allegations of misleading financial statements.

Yet her own disclosure history shows a pattern of delayed reporting, unexplained changes, and missing information spanning more than a decade. These aren’t minor oversights, but substantial, recurring issues involving properties worth millions and mortgages totaling hundreds of thousands of dollars.

A Cry for Accountability

Financial disclosure laws exist for a reason: to ensure transparency and prevent conflicts of interest among public officials. These aren’t burdensome regulations but essential safeguards of public trust.

When the state’s top legal officer demonstrates a decade-long pattern of disclosure problems, it undermines confidence in the very system she’s charged with upholding.

The Attorney General’s office has maintained silence in response to our detailed questions about these discrepancies. That silence becomes more deafening with each new revelation.